Hotcoin Research | When Macro Factors Become Pricing Logic: Prospective Analysis of Macro Variables in the Crypto Market in 2026

Introduction: The Importance of Macro Factors in the Cryptocurrency Market

The current volatility in the crypto market cannot be explained solely by “narrative heat” or “on-chain innovation.” Crypto assets are increasingly behaving like macro-sensitive risk assets, repeatedly influenced by interest rates, inflation, US dollar liquidity, regulatory frameworks, geopolitics, and institutional capital inflows and outflows.

The same on-chain data can reflect capital inflows when interest rate expectations rise, or signal risk contraction when tariff threats and geopolitical frictions intensify. Similarly, ETF capital inflows may act as long-term structural additions when regulatory channels are smooth, yet turn into short-term exits during periods of heightened policy uncertainty. Macro variables are no longer background noise; they have become the core engine shaping market trends, drawdown depth, and price structure.

This article analyzes the transmission mechanisms and impact pathways through which macro factors influence the crypto market. It identifies the key macro variables likely to affect crypto markets in 2026 and examines their potential evolution and market impact. The goal is to provide investors with a clearer analytical framework for identifying the origins of trends amid rising macro noise, understanding why volatility emerges, why capital gravitates toward more deterministic assets, and which variables require immediate reassessment when conditions shift. This framework aims to support more informed positioning and risk exposure decisions.

I. Historical Review of the Impact of Macro Variables on the Crypto Market

In the early stages of the cryptocurrency market, the influence of macro factors was not yet clearly visible, and crypto assets were driven primarily by internal supply–demand dynamics and technological progress. However, as market capitalization expanded and institutional participation increased, cryptocurrencies gradually came to be regarded as high-risk investment assets, and their price movements became increasingly connected to the macroeconomic environment. As a result, crypto market fluctuations are now closely linked to broader macro conditions. The following outlines the typical transmission paths through which major macro variables affect the cryptocurrency market.

Interest Rates and Liquidity

Interest rates determine the tightness of the monetary environment, which in turn shapes global liquidity conditions and risk appetite. When interest rates decline or liquidity expands, investors become more willing to allocate capital to high-risk assets, and funds tend to rotate from low-yield bonds into equities, crypto assets, and other risk categories. Conversely, rising risk-free interest rates in a high-rate environment weaken investor incentives to allocate capital to crypto assets.

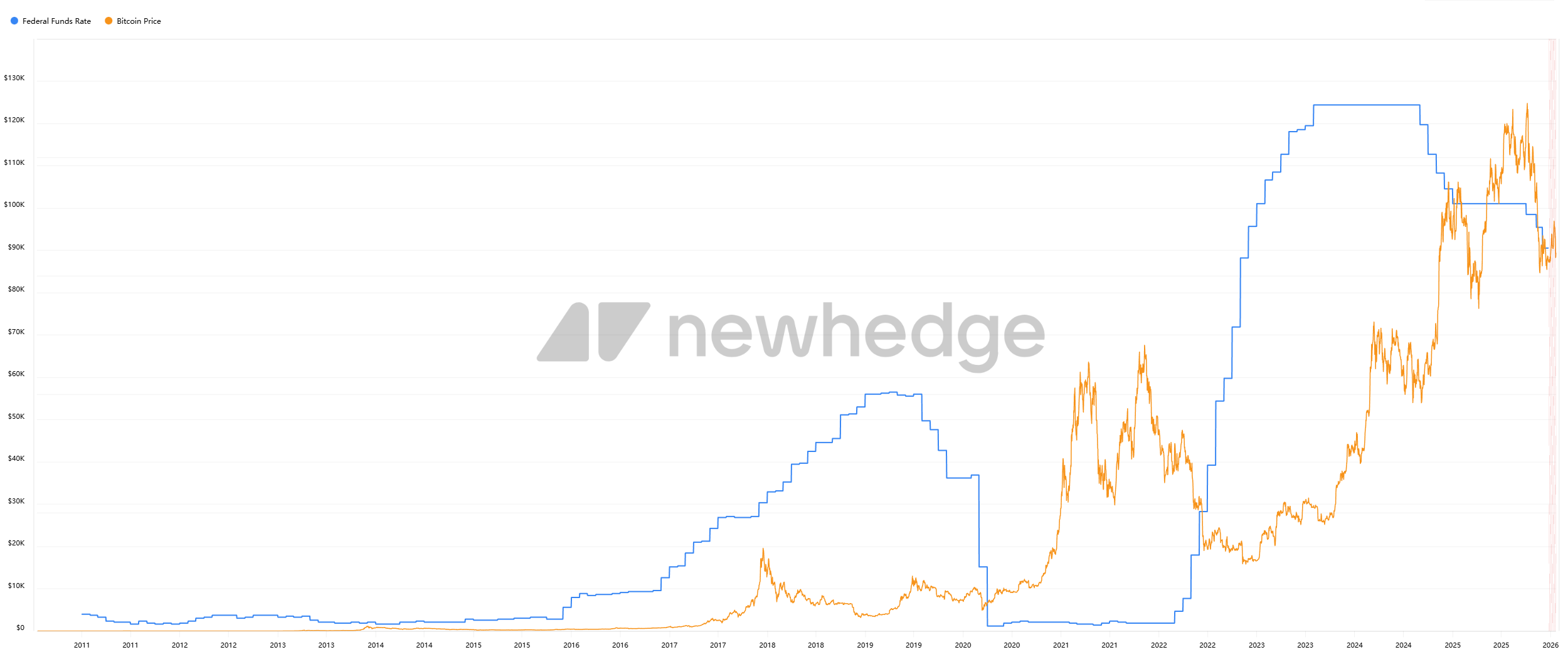

The ultra-low interest rate environment of 2020–2021 fueled a broad risk-asset boom, while the rapid rate hikes beginning in 2022, with policy rates exceeding 5%, sharply tightened liquidity and placed sustained pressure on the crypto market. In the second half of 2024, the Federal Reserve began a rate-cut cycle, and by the end of 2025, interest rates had declined from 3.5% to the 3% range. Market expectations now point to further moderation toward approximately 3.25% in 2026.

Interest rates and liquidity can therefore be considered among the most structurally influential macro factors shaping crypto market dynamics in recent years.

Source: https://newhedge.io/bitcoin/bitcoin-vs-federal-funds-rate

Inflation and Economic Growth

Inflation levels influence the direction of monetary policy and are closely linked to the purchasing power of fiat currencies and investors’ psychological expectations. In high-inflation environments, central banks typically tighten policies, which suppressed the cryptocurrency market in 2022. At the same time, inflation has led some investors to view Bitcoin as a form of “digital gold” for hedging inflation risk. However, this safe-haven narrative did not materialize during the high-inflation period of 2021–2022, as the negative effects of policy tightening outweighed the benefits of safe-haven status.

Economic growth cycles also indirectly affect cryptocurrency investment by influencing corporate and household wealth and overall risk preferences. The downturn in the crypto market between 2022 and 2023 was driven in part by monetary tightening amid elevated inflation and by slowing global economic growth and rising recession expectations, which weakened speculative sentiment. Overall, inflation dynamics and economic cycles exert a medium-term influence on the cryptocurrency market by shaping the policy environment and risk appetite, and these effects often intertwine with interest rate policy.

Regulatory Policies and Legal Environment

Regulatory factors exert a significant influence on the cryptocurrency market by reshaping behavioral norms, capital inflows and outflows, and expectations around market legitimacy. Constructive regulation, such as clarifying legal status and approving new investment pathways, tends to enhance investor confidence and attract incremental capital. In contrast, strict regulatory crackdowns, such as trading bans or the prosecution of industry participants, can trigger market sell-offs and heightened risk aversion.

Between 2021 and 2023, regulatory enforcement actions by US authorities against certain crypto projects, along with delays in ETF approvals, placed sustained pressure on market sentiment. From 2024 to 2025, regulatory frameworks introduced across multiple jurisdictions began to provide greater clarity and stability. For example, Europe’s MiCA framework initiated the implementation of unified regulatory standards in 2025, while the US passed the Stablecoin Act (GENIUS Act) in the same year, establishing standardized approval pathways for exchange-traded products.

These developments have improved compliance and transparency and are generally viewed by the market as long-term structural benefits. Regulatory impacts tend to manifest in the short term through policy-driven price reactions, while over longer horizons they shape industry structure and capital allocation patterns, making regulation a decisive macro variable alongside monetary policy.

Institutional Fund Flow and Market Structure

With the opening of compliant investment channels, such as ETFs, and the participation of listed companies and institutional investors, the fund structure and pricing mechanisms of the cryptocurrency market have undergone significant changes. Institutional capital typically operates on a large scale and favors mainstream assets, thereby amplifying overall market trends.

For example, the first wave of US spot Bitcoin ETFs between 2024 and 2025 generated substantial capital inflows. According to available data, Bitcoin ETFs and listed company accumulation strategies, such as those adopted by MicroStrategy, contributed nearly 44 billion USD to net buying demand in 2025 alone. Institutional participation has also driven structural shifts within the market. Bitcoin’s dominance of total crypto market capitalization rose to over 60% in 2025, well above the peak levels observed in previous cycles, indicating a growing concentration of capital in top-tier assets, particularly Bitcoin.

Stablecoins and Capital Flow

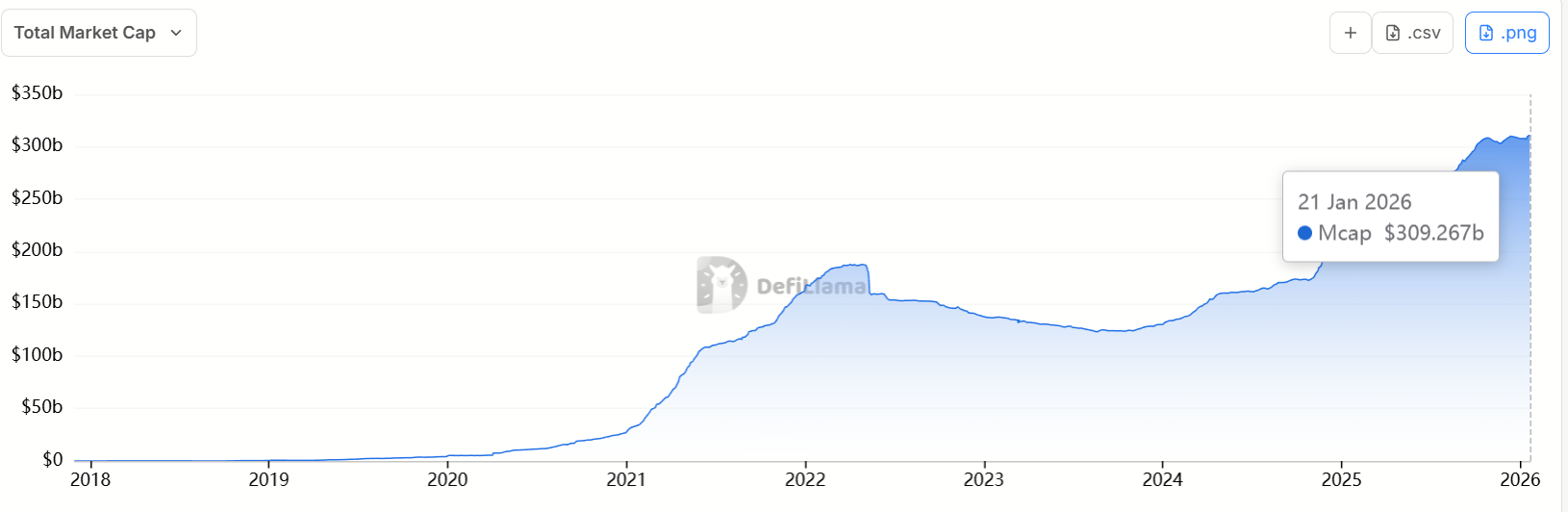

As a key infrastructure component of the crypto market, the issuance and circulation of stablecoins directly reflect the liquidity “reservoir” within the ecosystem and are also influenced by broader macroeconomic conditions. In bull markets, capital inflows typically drive rapid expansion in stablecoin market capitalization, while in bear markets, demand for stablecoins declines and overall supply contracts.

Changes in stablecoin supply often lead or move in tandem with broader capital flow dynamics, reflecting the pace at which funds enter and exit the market. During the 2020–2021 bull market, the supply of major stablecoins such as USDT and USDC expanded from less than 30 billion USD to more than 150 billion USD by the end of 2021. In contrast, during the 2022 bear market, total stablecoin market capitalization declined modestly and stabilized around 130 billion USD. As a new market cycle emerged between 2024 and 2025, stablecoin issuance resumed its expansion, with total global stablecoin market value exceeding 300 billion USD, representing growth of approximately 75% compared with one year earlier.

Source: https://defillama.com/stablecoins

II. Analysis of the Impact of Macro Variables on the Cryptocurrency Market

Variable 1: Global Interest Rates, Inflation, and Liquidity Outlook

Monetary Policy – Impact: ★★★★★

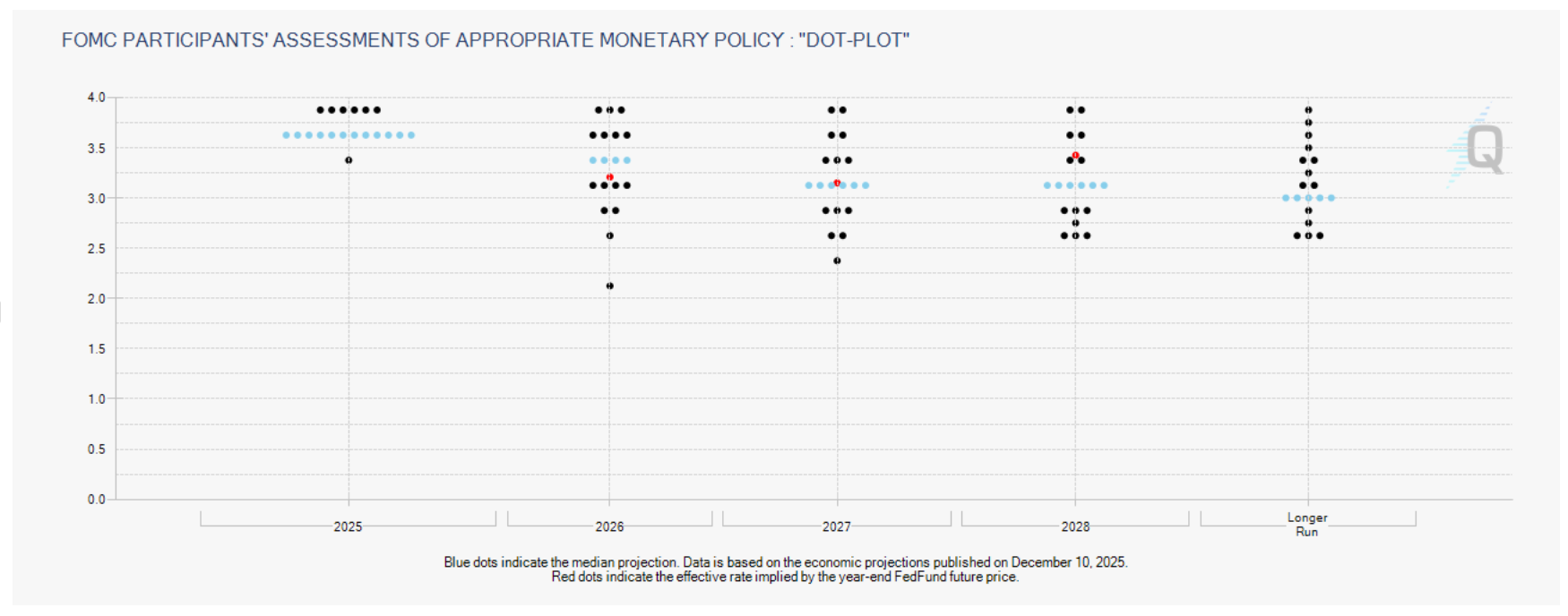

Entering 2026, the global monetary policy environment is approaching a critical inflection point. The Federal Reserve transitioned from tight to gradually easing conditions between 2024 and 2025. After raising interest rates continuously and pushing the federal funds rate to 5.25%, the Fed began cutting rates toward the end of 2024. In 2025, interest rates were reduced three times, bringing the policy range down to 3.5%–3.75%, the lowest level in three years.

In 2026, the Federal Reserve is expected to continue easing at a measured pace. Current dot-plot projections indicate that the federal funds rate may decline to approximately 3.25% by year-end. It is also worth noting that Chair Jerome Powell’s term is scheduled to end in May 2026, and a potential leadership transition could introduce additional policy uncertainty. Overall, assuming no major inflation surprises, the US monetary environment in 2026 is likely to be materially more accommodative than in the previous two years. While there are no clear signals pointing to a return to quantitative easing, liquidity conditions are no longer tightening, which is supportive of risk asset performance.

Turning to other major central banks, both the European Central Bank and the Bank of England are expected to conclude their tightening cycles during the 2024–2025 period. In 2026, they are likely to shift toward a wait-and-see stance or begin gradual rate cuts, though the pace of easing may lag the Federal Reserve's. The Bank of Japan remains an exception. After maintaining near-zero or negative interest rates for an extended period, it initiated rate increases in 2025, but overall policy rates remain low and may follow a relatively independent trajectory in 2026.

Taken together, global interest rates are expected to move into a downward channel in 2026, particularly in core markets such as the United States. This shift should help release liquidity and reduce the opportunity cost of holding risk assets. However, persistently elevated inflation remains a key downside risk. If inflation proves more sticky than expected, central banks may face renewed constraints from price pressures, limiting their ability to ease policy meaningfully.

.

Source: https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

Inflation and Economic Outlook – Strength of Impact: ★★★★☆

The prevailing expectation for 2026 is that inflation in major economies will continue to ease, returning to or even falling slightly below target levels. For example, the Federal Reserve’s latest projections indicate that US PCE inflation may decline to approximately 2.4% in 2026, close to the long-term target of 2%. Cooling inflation allows central banks to halt rate hikes, which is generally supportive of risk assets, including cryptocurrencies. If inflation remains moderate or undershoots expectations in 2026, additional room may emerge for unexpected rate cuts or liquidity support, further lifting market valuations. Recent market behavior illustrates this dynamic, as periods of softer-than-expected inflation data toward the end of 2025 coincided with synchronized gains in Bitcoin and US equities.

From a growth perspective, the global economy is expected to expand at a moderate pace in 2026. The IMF projects that major developed economies will grow by around 2% across 2025–2026, with the United States modestly outperforming Europe. A low-growth but non-recessionary environment typically supports relatively stable policy settings and sustained market confidence. JP Morgan’s outlook similarly anticipates that major economies will maintain stable growth or operate slightly above potential levels. However, should a major financial risk event unexpectedly materialize in 2026, risk assets, including cryptocurrencies, could face short-term pressure. Historically, however, recessionary conditions have prompted central banks to adopt more aggressive monetary easing, which has often laid the groundwork for subsequent bull markets.

Key risks requiring ongoing monitoring include inflation volatility driven by energy price shocks or geopolitical tensions, as well as market instability stemming from leadership changes at major central banks or miscommunication of policy intentions. If these risks remain contained, accommodative monetary conditions are likely to become a meaningful tailwind for the cryptocurrency market in 2026.

Variable 2: Regulatory Policy Trends and Market Structure Changes

Regulatory and Legal Environment – Impact: ★★★★☆

2025 is widely regarded as the “Year of Crypto Regulation.” Major jurisdictions introduced or implemented key regulatory frameworks, accelerating the industry’s transition from regulatory gray zones toward compliance. The continued evolution of regulatory policy in 2026 remains one of the most influential variables shaping the crypto market. Overall, global regulation is moving toward greater clarity and standardization, which supports improved long-term market expectations. However, differences in implementation pace across regions during the transition period may still generate short-term volatility in capital flows and market sentiment.

On the US side, July 2025 marked the passage of the country’s first federal stablecoin legislation, the GENIUS Act. Under the framework, regulatory agencies are expected to release detailed implementation rules before July 2026. If these rules are clearly defined and effectively executed, they could significantly enhance transparency, expand bank participation in stablecoin issuance, and increase both the supply capacity and structural depth of the crypto market. This may also contribute to a more diversified stablecoin landscape. Market data already reflects this trend: USDT’s market share declined from approximately 86% in 2020 to around 58% in 2025, while USDC’s share increased to about 25%, and newer stablecoins such as USD1 and PYUSD gained traction.

Beyond stablecoin legislation, US lawmakers advanced discussions around the CLARITY Act in 2025, aiming to more clearly distinguish between security tokens and commodity tokens. The key question in 2026 is whether this legislation will move from proposal to implementation. Although political uncertainty remains, market attention toward the CLARITY Act is high, and its passage would likely act as a meaningful positive catalyst for asset prices.

At the regulatory agency level, the US Securities and Exchange Commission underwent a notable shift in 2025. The new leadership introduced the “Project Crypto” initiative, signaling a comprehensive review of rules governing crypto-related securities. In September 2025, the SEC approved unified listing standards for spot-commodity ETFs, significantly lowering regulatory barriers to crypto-linked ETF products. As a result, a broader range of crypto ETFs and ETPs is expected to emerge in 2026, including multi-asset basket products and ETH spot ETFs. This expansion would further integrate digital assets into mainstream investment portfolios.

At the same time, regulatory positions toward areas such as DeFi, counterfeit assets, and certain protocol-level activities remain less defined. Should targeted regulatory constraints emerge in 2026, affected assets could face pricing pressure. However, enforcement actions are expected to remain cautious until broader legislative clarity, particularly around the CLARITY Act, is achieved.

In other regions, the European Union fully implemented the Markets in Crypto-Assets Regulation (MiCA) in 2025, and regulatory conditions are expected to remain stable and supportive of compliance in 2026. The EU also updated its Anti-Money Laundering framework, extending Travel Rule requirements to crypto transactions. While these measures enhance transparency and reduce illicit capital flows, they also increase compliance pressure on non-conforming platforms.

Major Asian economies strengthened their crypto regulatory frameworks in 2025 as well. Japan refined exchange and custody oversight, South Korea advanced comprehensive digital asset legislation, Hong Kong expanded exchange licensing and introduced stablecoin regulations, and Singapore implemented a formal crypto licensing regime under the Financial Services and Markets Act, entering a fully regulated phase in 2026. Emerging markets, including parts of the Middle East and Latin America, have also adopted more crypto-friendly policies or attracted crypto firms, positioning themselves as potential beneficiaries of global crypto capital spillovers.

In summary, regulatory developments are likely to exert a more constructive influence on the cryptocurrency market in 2026. Clearer rules reduce structural uncertainty and support industry development, although regulatory trajectories must continue to be closely monitored, as policy shifts in any major jurisdiction can rapidly transmit across global markets and be reflected in asset prices.

Variable 3: Institutional Investment and the Evolution of Market Structure

Institutional Funds and Investment Vehicles – Impact: ★★★★☆

2026 may mark a year of significant institutionalization of cryptocurrency assets. First, with the emergence of US spot Bitcoin ETFs and Ethereum futures and spot ETFs, traditional financial institutions are incorporating crypto assets into their asset allocations at an unprecedented pace. ETFs and related products have lowered the threshold for crypto investment, enabling conservative institutions such as insurance companies, pension funds, and university endowments to begin allocating to Bitcoin through ETFs, small-scale exploratory positions, and similar channels.

According to available data, Bitcoin ETFs listed in the US in 2025 generated approximately $30 billion in incremental demand. This figure is expected to continue rising in 2026, while investable asset classes are likely to expand from BTC and ETH toward diversified crypto portfolio ETFs, DeFi-focused ETFs, and other structured products. A substantial volume of capital from traditional securities markets continues to flow into crypto through ETFs, forming a persistent source of buying support for Bitcoin and other mainstream crypto assets.

From a structural perspective, ETFs have reshaped portfolio construction, increasing diversification within institutional portfolios and reducing systemic concentration risk.

Secondly, it has become increasingly common for publicly listed companies to hold crypto assets on their balance sheets. As of January 21, 2026, MicroStrategy held 709,715 BTC, accounting for approximately 3.38% of the total Bitcoin supply. The growing inclusion of digital assets on corporate balance sheets has enhanced market recognition of crypto as a strategic asset class.

At the same time, emerging Digital Asset Vaults (DATs) that have gone public have contributed notable buying pressure between 2024 and 2025, with expectations for continued expansion in 2026. However, it should also be noted that when asset prices rise significantly, some holding entities may engage in profit-taking or reduce positions, introducing marginal selling pressure.

Overall, rising institutional ownership has strengthened Bitcoin’s store-of-value characteristics and improved market stability, while also introducing a degree of cyclicality, as institutions tend to buy during drawdowns and rebalance during periods of elevated prices—potentially dampening extreme volatility.

Another major consequence of institutional participation is the transformation of market structure and volatility dynamics. In 2025, Bitcoin dominance rose above 60%, accompanied by reduced volatility. This trend reflects institutional preference for large-cap, high-liquidity assets, concentrating capital in BTC and ETH rather than speculative or low-quality tokens.

Meanwhile, the maturation of derivatives markets and the broader adoption of options-based hedging strategies have further suppressed short-term price swings. Looking ahead, institutional ownership of Bitcoin is expected to continue increasing in 2026, while Ethereum is likely to maintain steady growth.

For small- and mid-cap tokens, 2026 may represent a market of two extremes. On one hand, macro recovery supports expansion in overall market capitalization, with Bitcoin leading the market into a new phase of selective growth. On the other hand, tighter regulatory clarity acts as a filter for lower-quality or speculative assets.

As a result, the sector is unlikely to experience the broad-based speculative excess seen in 2017 or 2021. Instead, the market may exhibit a combination of resilience and divergence: high-quality projects benefit from structural inflows, while long-tail, high-risk tokens remain under pressure.

In summary, driven by institutional adoption, the cryptocurrency market in 2026 is likely to be increasingly shaped by compliant capital and professional investment frameworks, with blue-chip assets and high-quality projects at the core. Speculative excess is expected to narrow, while market structure becomes more disciplined and differentiated.

Variable 4: Geopolitics and Global Capital Flows

Geopolitical Events and Macro Risks – Impact: ★★★☆☆

In addition to economic and regulatory factors, geopolitical developments and major macro risk events can indirectly affect the cryptocurrency market by shaping investor risk appetite and global capital flows. In 2026, the following dimensions warrant close attention:

Geopolitical uncertainty, such as armed conflicts, trade frictions, and regional instability, often triggers short-term risk-off sentiment in global markets. Capital typically flows into traditional safe-haven assets such as the US dollar and gold, while higher-risk assets, including equities and cryptocurrencies, come under pressure.

However, prolonged or structural geopolitical stress—including economic sanctions, capital controls, or sustained currency depreciation can also generate localized demand for crypto assets. In such environments, individuals and institutions may seek alternative channels for asset transfer, value preservation, or inflation hedging. For example, following the Russia–Ukraine conflict, the Russian ruble depreciated sharply, while local Bitcoin trading volumes increased significantly.

Potential geopolitical risk factors in 2026 include escalating tensions in Eastern Europe and the Middle East, renewed geopolitical frictions involving the US, Venezuela, or Greenland, expanded sanctions regimes, and uncertainty surrounding US midterm elections. In the short term, these developments would likely increase global risk aversion and weigh on crypto markets. Over the longer term, however, the neutral and borderless nature of crypto assets may allow them to function as alternative liquidity channels amid global financial fragmentation, reinforcing their role in hedging systemic risks.

The US Dollar Index (DXY) typically exhibits an inverse relationship with crypto asset performance. A strengthening US dollar often coincides with capital outflows from emerging markets and tighter global liquidity, both of which are unfavorable for non-dollar assets such as cryptocurrencies. Conversely, a weakening dollar tends to improve relative demand for crypto assets.

If the Federal Reserve cuts interest rates in 2026 while Europe lags in policy easing, the US dollar may weaken moderately. This could reduce exchange-rate pressure on non-US investors and increase the incentive to allocate capital to crypto assets. When specific countries experience currency crises, regional crypto capital flows may undergo structural shifts, as individuals and firms in high-inflation environments increase their crypto holdings to preserve purchasing power. Such dynamics may also introduce new users and incremental capital into the global crypto market.

Capital controls and tax regimes play a significant role in shaping regional crypto activity. For example, India’s high taxation and strict regulatory framework previously led to a sharp contraction in domestic crypto trading volumes. If these policies are relaxed in 2026, latent demand could be released. Conversely, if crypto-friendly jurisdictions tighten regulations, corresponding market activity may contract.

At the same time, governments are increasingly strengthening oversight of cross-border capital flows, particularly in the areas of anti-money laundering and tax enforcement. Crypto assets can serve legitimate compliance-based cross-border transfer needs—such as stablecoin use for remittances —but may also be misused. In 2025, many jurisdictions intensified AML enforcement, a trend expected to become more normalized in 2026. In the short term, this may affect demand for privacy-focused or anonymity-oriented tokens.

Overall, the impact of geopolitical and macro risk events is typically sudden and short-term, making precise forecasting difficult. As a result, investors should incorporate structured risk management strategies, including moderate allocations to relatively mature assets such as gold and Bitcoin as potential hedges against geopolitical uncertainty.

III. The Crypto Market Outlook for 2026 Under the Influence of Multiple Macro Variables

Based on the macro analysis above, we can outline potential trends for the cryptocurrency market in 2026. Naturally, the future remains uncertain. The scenarios below are intended to provide a structured framework for thinking, while investors should continuously adjust expectations based on real-time data and evolving conditions.

Benchmark Scenario (Macro Stability and Gradual Easing)

In the benchmark scenario, the global economy continues to grow at a moderate pace. Major central banks, led by the United States, maintain interest rates around 3% following limited rate cuts, while inflation remains close to target levels. No significant negative regulatory shocks emerge, and newly introduced regulations are gradually implemented, allowing markets to adapt smoothly.

Under these conditions, the cryptocurrency market is expected to extend its upward trajectory from 2025 and transition into a more mature growth phase. Bitcoin may continue setting new highs on the foundation established in 2025, supported by sustained ETF inflows and the gradual realization of supply-reduction effects. Although the pace of annual gains may moderate compared with 2025, overall appreciation could remain meaningful.

Ethereum is expected to benefit from ongoing technological upgrades and increased institutional allocation. While it may outperform Bitcoin in certain periods, its overall performance is likely to remain broadly aligned with market trends. Within the broader altcoin segment, projects with clear application value and strong compliance prospects are likely to attract capital, while purely speculative tokens may see shorter-lived and more limited rallies, even in a generally rising market environment.

The stablecoin market is expected to continue expanding and could surpass the 400 billion USD threshold. Investor sentiment under this scenario remains constructive but increasingly rational, with market volatility at moderate levels and extreme exuberance or panic becoming less frequent.

Optimistic Scenario (Macro Surprise and Technological Breakthrough)

In the optimistic scenario, several positive developments compound on the benchmark outlook. Inflation declines more rapidly than expected, potentially even signaling mild deflation, prompting major central banks to restart quantitative easing in the second half of 2026. In parallel, the US Congress successfully passes key crypto legislation, such as the CLARITY Act, while regulatory coordination between agencies improves and long-standing gray areas are resolved.

At the same time, large technology companies may launch high-impact applications that bring blockchain technology to hundreds of millions of users, and pension funds in Europe, the US, and other regions begin allocating capital to Bitcoin. Together, these factors could ignite renewed “FOMO” sentiment and push the market into an accelerated expansion phase.

Under this scenario, Bitcoin prices could experience a parabolic rise reminiscent of 2017 or 2021. Ethereum and other major assets would likely rally in tandem, potentially accompanied by short-term surges in speculative segments. Total market capitalization could exceed previous-cycle multiples and move decisively into the mainstream of global financial assets. However, such an overheated environment would be difficult to sustain, and any shift in macro or policy conditions could trigger sharp corrections.

Pessimistic Scenario (Macro Shock and Risk Events)

In the pessimistic scenario, adverse factors materialize simultaneously. Inflation proves sticky, delaying interest-rate cuts; global financial markets experience systemic stress; crypto-related legislation in the US stalls or reverses; geopolitical tensions escalate; or policy uncertainty increases following elections or trade disputes.

Under these conditions, liquidity tightens, and risk aversion rises, leading to significant drawdowns in Bitcoin prices. Institutional investors may reduce exposure, including through crypto ETFs, due to losses elsewhere or a sharp deterioration in risk appetite, resulting in net capital outflows. If major industry institutions encounter operational or financial stress, market panic could intensify.

In this scenario, speculative tokens would likely suffer the deepest declines, while Ethereum and other major assets would also fall alongside the broader market. For long-term investors, such periods may offer opportunities to accumulate high-quality assets at discounted levels. Short-term traders, however, would need to prioritize risk management and stop-loss discipline.

Most Likely Path

The most probable outcome lies between the benchmark and optimistic scenarios, with a bias toward gradual improvement. Current indicators suggest that macro conditions are gradually becoming more supportive, regulatory frameworks are steadily taking shape, and industry-specific innovation is continuing to build momentum.

After Bitcoin reached new highs in 2025 without triggering the kind of extreme speculative bubble seen in earlier cycles, the market appears to retain room for further upside in 2026. Investor behavior has become more mature and disciplined following the 2022–2023 downturn. Provided no major systemic “black swan” events occur, the overall market trend in 2026 is likely to remain constructive, with milder fluctuations than in previous cycles.

Market performance may follow an “oscillating upward” pattern: the first quarter could be influenced by macro uncertainty or profit-taking, the middle of the year may benefit from declining interest rates and clearer regulatory implementation, and additional technological catalysts in the fourth quarter could generate renewed momentum. From a longer-term perspective, 2026 may serve as the foundation for the next major crypto cycle.

Conclusion

The cryptocurrency market in 2026 stands at a new inflection point. Macroeconomic shifts and policy developments will continue to shape the trajectory of this emerging asset class. Interest-rate dynamics, regulatory clarity, institutional participation, and geopolitical factors are increasingly intertwined, reinforcing the integration of crypto markets with the broader global financial system.

On one hand, this integration demands that investors adopt a macro-aware, cross-market perspective. On the other hand, it signals that the crypto industry is maturing: price movements are no longer driven solely by speculative enthusiasm, but are increasingly linked to economic fundamentals and institutional behavior.

For investors, 2026 is likely to present both opportunities and challenges. While the easing of monetary conditions and clearer regulations may create favorable tailwinds, market unpredictability and risk events remain ever-present. A balanced approach — cautious yet forward-looking, rational yet open to innovation — will be essential.

Looking ahead, the cryptocurrency market will continue to evolve. Its underlying drivers — user growth, institutional recognition, regulatory normalization, and technological advancement — are stronger than ever. These fundamentals provide a solid foundation for crypto assets to advance toward a broader, more established role in the global financial landscape.

About Us

Hotcoin Research, the core research and investment arm of Hotcoin Exchange, is dedicated to turning professional crypto analysis into actionable strategies. Our three-pillar framework—trend analysis, value discovery, and real-time tracking—combines deep research, multi-angle project evaluation, and continuous market monitoring.

Through our Weekly Insights and In-depth Research Reports, we break down market dynamics and spotlight emerging opportunities. With Hotcoin Selects, our exclusive dual-screening process powered by both AI and human expertise, we help identify high-potential assets while minimizing trial-and-error costs.

We also engage with the community through weekly livestreams, decoding market hot topics, and forecasting key trends. Our goal is to empower investors of all levels to navigate cycles with confidence and capture long-term value on Web3.

Risk Disclaimer

The cryptocurrency market is highly volatile, and all investments carry inherent risks. We strongly encourage investors to stay informed, assess risks thoroughly, and follow strict risk management practices to protect their assets.

Connect with Us

X: x.com/HotcoinAcademy

Email: labs@hotcoin.com

Đề xuất đọc

Xem thêm

Hotcoin Research | Uncovering the Influence of Macroeconomics: Correlation Analysis between US Economic Indicators and Crypto Market Fluctuations

In-depth Research

Hotcoin Research | Kaspa: Blockchain to BlockDAG, Pioneering Next-Gen Industrial Infrastructure

In-depth Research

Hotcoin Research | An Overview of the Hottest AI Agent Frameworks: Technological Breakthroughs and the Integration of Token Economies

In-depth Research