Hotcoin Research | "Threat" Before "Action": How Geopolitical Risk Is Priced in Crypto Markets – Transmission Mechanisms and Trend Outlook

TL;DR

Background: As geopolitical risks escalate, the crypto market has increasingly behaved like a high-beta risk asset, becoming deeply embedded in the global macro cycle.

Quantitative Framework: The GPR Index comprises two components: “Threat” and “Action.” Historical analysis shows that negative market impacts are mainly driven by the “Threat” component.

Transmission Mechanism: Risk appetite shifts | Inflation and interest rate cut expectations | Market structure amplification.

Drivers of High Beta: Strengthening correlation among risk assets + high leverage liquidation cascades + endogenous liquidity contraction.

Trend Outlook:

-

Base scenario: shock repair and gradual stabilization

-

Pessimistic scenario: double-bottom formation

-

Optimistic scenario: high-volatility overshoot followed by a rebound.

Implication: Investors should incorporate geopolitical risk into a unified macro framework and dynamically assess its impact on risk premiums and liquidity conditions.

I. Overview of Geopolitical Risks

-

What Does Geopolitical Risk Mean?

Geopolitical risks are often described as the market impact of major breaking news events. However, a more accurate understanding is that they represent a collection of events and expectations—including the escalation of war or conflict, terrorist attacks, sanctions and counter-sanctions, diplomatic confrontations, disruptions to key shipping routes, trade frictions, tariff escalations, and other developments that collectively create uncertainty about the future.

The key aspect of geopolitical risk is not the event itself, but the market’s repricing of the probability of future outcomes. In this sense, the GPR Index functions as a macro-level risk premium generator. It may not surge every day, but when it rises, markets typically respond with higher risk discounts, more conservative risk preferences, and tighter capital conditions.

-

How to Quantify Geopolitical Risks?

The Geopolitical Risk Index (GPR Index), compiled by US Federal Reserve economists Dario Caldara and Matteo Iacoviello, measures the proportion of negative geopolitical events or threats discussed in international newspapers and magazines since 1900. The dataset is constructed using content from the top 10 international newspapers.

The Geopolitical Risk Index is designed to measure changes in global geopolitical risk. It is commonly used to assess the potential impact of factors such as political instability, conflict, war, and policy shifts on a country's or region's economic activity and financial markets. Importantly, the framework further divides geopolitical risk into two more transactional stages.

-

Threats: The stage where risks are emerging but have not yet materialized. During this phase, words such as threats, warnings, concerns, risks, and tensions appear more frequently in media coverage. When threats rise, markets tend to price in possibilities and expectations first, typically reflected in rising panic indicators, a strengthening US dollar and gold, and the emergence of an oil risk premium.

-

Actions: The stage where risks have already occurred or significantly escalated. The share of reports describing actual events—such as the outbreak of war, escalation of conflict, or terrorist attacks—rises. At this stage, markets begin to price real economic shocks related to supply, demand, policy, and growth, and volatility often intensifies, increasing the likelihood of cross-asset chain reactions.

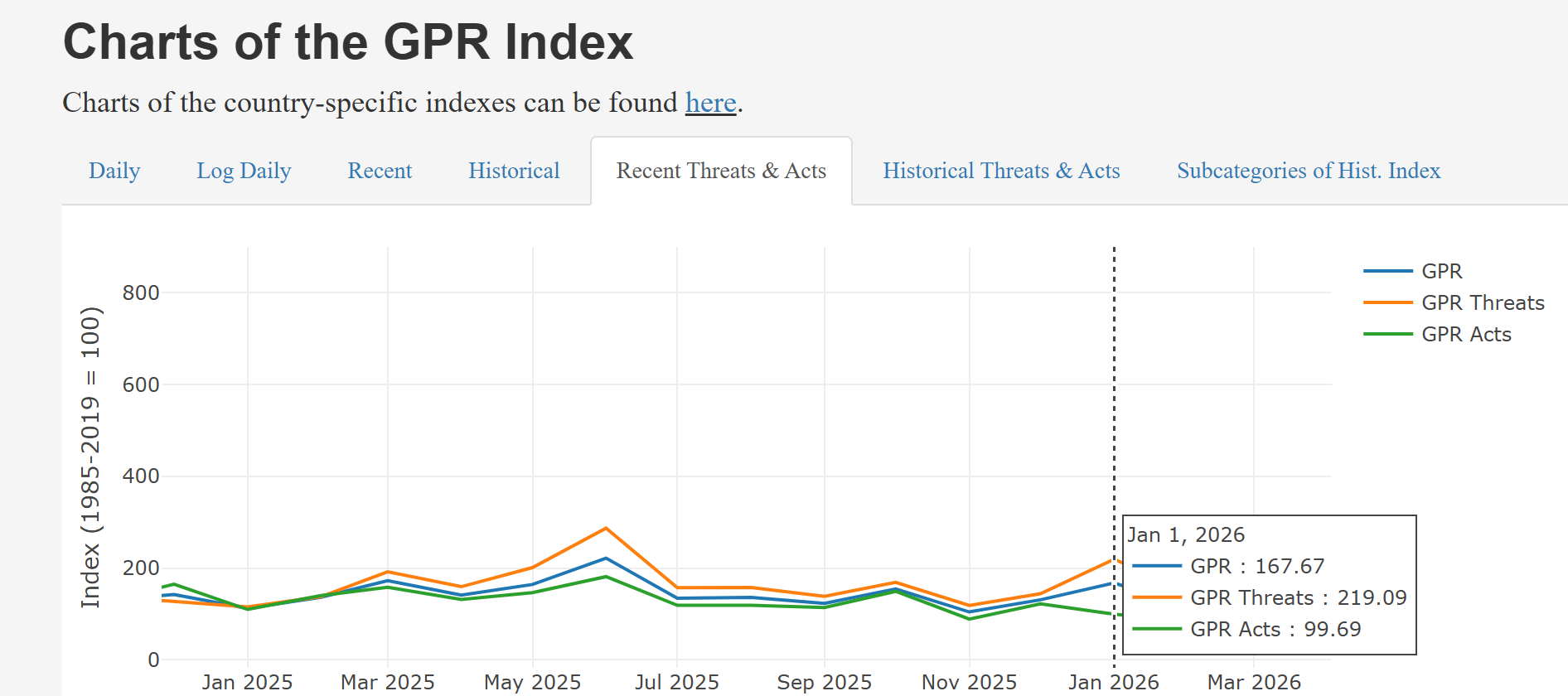

According to data from the MacroMicro platform, the global geopolitical risk “Threat” index rose significantly in January 2026, reaching 219.09. When the GPR index rises, the market’s initial reaction is typically to reduce risk exposure before evaluating potential bottom-fishing opportunities. This dynamic is usually reflected in higher volatility (such as a rising VIX), declining risk assets, and stronger demand for safe-haven and cash assets.

Source: https://www.matteoiacoviello.com/gpr.htm

II. The Impact and Transmission of Geopolitical Risks

A rise in geopolitical risk (GPR) does not directly lead to volatility in the cryptocurrency market. Instead, it first increases macro-level uncertainty, which is then transmitted through multiple channels, ultimately resulting in sharp co-directional fluctuations in the crypto market. This dynamic reflects the combined effect of macro pressure transmission and market structure amplification.

The upward movement of GPR mainly operates through the following four mechanisms:

-

Risk preference shift: VIX rises, credit spreads widen, and overall exposure to risky assets declines.

-

Energy and commodity shocks: Gold and oil prices increase, pushing inflation expectations higher.

-

Policy and liquidity repricing: Expectations for interest rate cuts are postponed, the US dollar strengthens, and long-term interest rates rebound.

-

Market structure amplification: Thin liquidity during weekends, highly leveraged derivatives positions, and forced liquidations can create cascading liquidation events.

These mechanisms together cause the cryptocurrency market to experience larger and more volatile moves than traditional equity markets, often in the same direction.

-

Risk Appetite Switching

The escalation of geopolitical conflicts typically triggers risk aversion. Safe-haven sentiment intensifies in the stock market, the volatility indicator VIX rises, and capital flows out of high-volatility assets into traditional safe-haven assets.

The VIX (Chicago Board Options Exchange Volatility Index) is a core indicator that measures the expected volatility of the US stock market over the next 30 days. It is calculated from S&P 500 index option prices and reflects implied market volatility rather than historical volatility. Because it tends to surge during market downturns, it is often called the “panic index.”

Its numerical range broadly reflects market sentiment:

-

Below 20 indicates stable optimism

-

20–30 indicates heightened vigilance;

-

Above 30 signals high panic;

-

A score above 40 reflects extreme panic, typically seen during major crises.

In March 2026, the VIX rose rapidly from around 14.5 at the beginning of the year to above 20, reflecting growing market concerns about military conflicts and energy supply chain disruptions. As a classic safe-haven asset, gold often sees strong buying interest in the early stages of geopolitical crises. Research from the World Gold Council shows that for every 100-point increase in the GPR index, the average gold price rises by approximately 2.5%. Spot gold also shows a strong positive correlation with the GPR index. When sovereign credit risks increase or macro conditions deteriorate, gold’s safe-haven characteristics can even outperform traditional reserve currencies.

-

Inflation and interest rate cut concerns

Escalating geopolitical conflicts in the Middle East often play a leading role in shaping oil prices and shipping expectations, heightening inflation concerns and forcing markets to scale back expectations for interest rate cuts, which places sustained pressure on overvalued and highly volatile assets.

The core driver of oil price fluctuations is the risk of supply disruptions, rather than sentiment alone. The security of key shipping routes—such as the Strait of Hormuz—directly affects the level of the geopolitical risk premium embedded in energy prices. If conflicts persist, they can create sustained inflationary pressure. While gold primarily reflects safe-haven demand arising from financial system uncertainty, oil prices more directly reflect the impact of conflicts on real-economic supply conditions and inflation. When markets begin to worry about supply chain disruptions, sanctions, and counter-sanctions, oil prices tend to be rapidly repriced.

Brent crude oil has recently risen sharply, recording a monthly increase of more than 20%. When geopolitical risks intensify, energy price shocks and market volatility often occur simultaneously, triggering risk appetite shifts and liquidity repricing. Rising oil prices strengthen concerns about persistent inflation and reduce the certainty of interest rate cuts. When market expectations shift from “imminent easing” to “higher for longer” interest rates, crypto assets—given their high volatility and strong reliance on liquidity conditions—often come under pressure first, particularly during periods of thin market liquidity.

Since the beginning of 2026, crude oil prices and the VIX have shown a strong positive correlation. Currently, both indicators are rising simultaneously, suggesting that soaring energy prices are directly contributing to growing market panic.

The price of BTC, often referred to as “digital gold,” shows a significant negative correlation with the VIX. In other words, the higher the level of market panic, the greater the selling pressure on Bitcoin. This dynamic occurs because inflationary pressure driven by rising crude oil prices strengthens expectations of persistently higher interest rates, delivering a double blow to risk assets such as Bitcoin while also weighing on the broader equity market, as reflected in the rise of the VIX.

-

Characteristics of the Encryption Market Structure

After macro pressure is transmitted to the crypto market through the first three channels, the crypto market's structural characteristics further amplify the impact. These structural features explain why the crypto market often experiences greater volatility than traditional risk assets during periods of geopolitical stress.

• 24/7 trading: Continuous trading makes weekends particularly vulnerable to macro shocks. With traditional markets closed, hedging tools are limited, and market depth becomes thinner.

• Derivatives and high leverage: The large share of leveraged derivatives means that falling prices can quickly trigger margin calls and forced liquidations, creating a cascading “passive selling” effect.

• Liquidity stratification: Liquidity is uneven across the market—between large and small exchanges, spot and perpetual markets, and mainstream versus long-tail tokens. When risk appetite contracts, liquidity tends to concentrate on top assets, while tail assets often experience sharper declines.

These mechanisms contribute to the “high beta” nature of the cryptocurrency market, meaning its volatility is driven largely by structural dynamics rather than purely by market sentiment.

It is also worth noting that when geopolitical conflicts are accompanied by sanctions, capital controls, or restrictions on the banking system, cryptocurrencies—due to their cross-border transferability and alternative settlement capabilities, may temporarily serve as local safe-haven assets, providing buying support. During the early stages of the Russia–Ukraine war, for example, there was increased fiat-to-crypto trading activity and a noticeable rise in related demand.

However, while this channel can provide short-term support, it is usually insufficient to reverse a broader downturn driven by global macro risk aversion—unless reinforced by stronger structural narratives such as persistent inflation or sovereign debt crises.

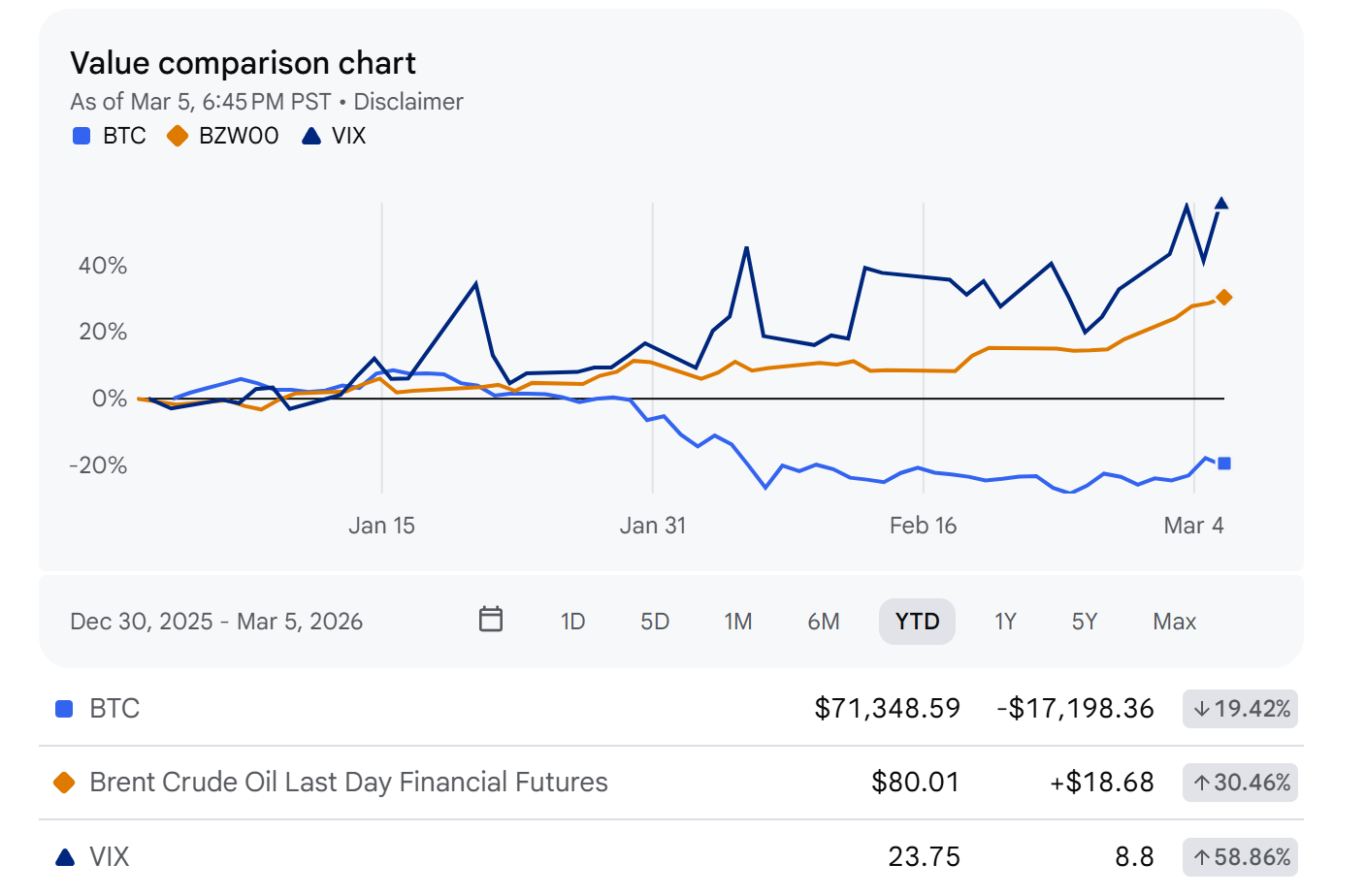

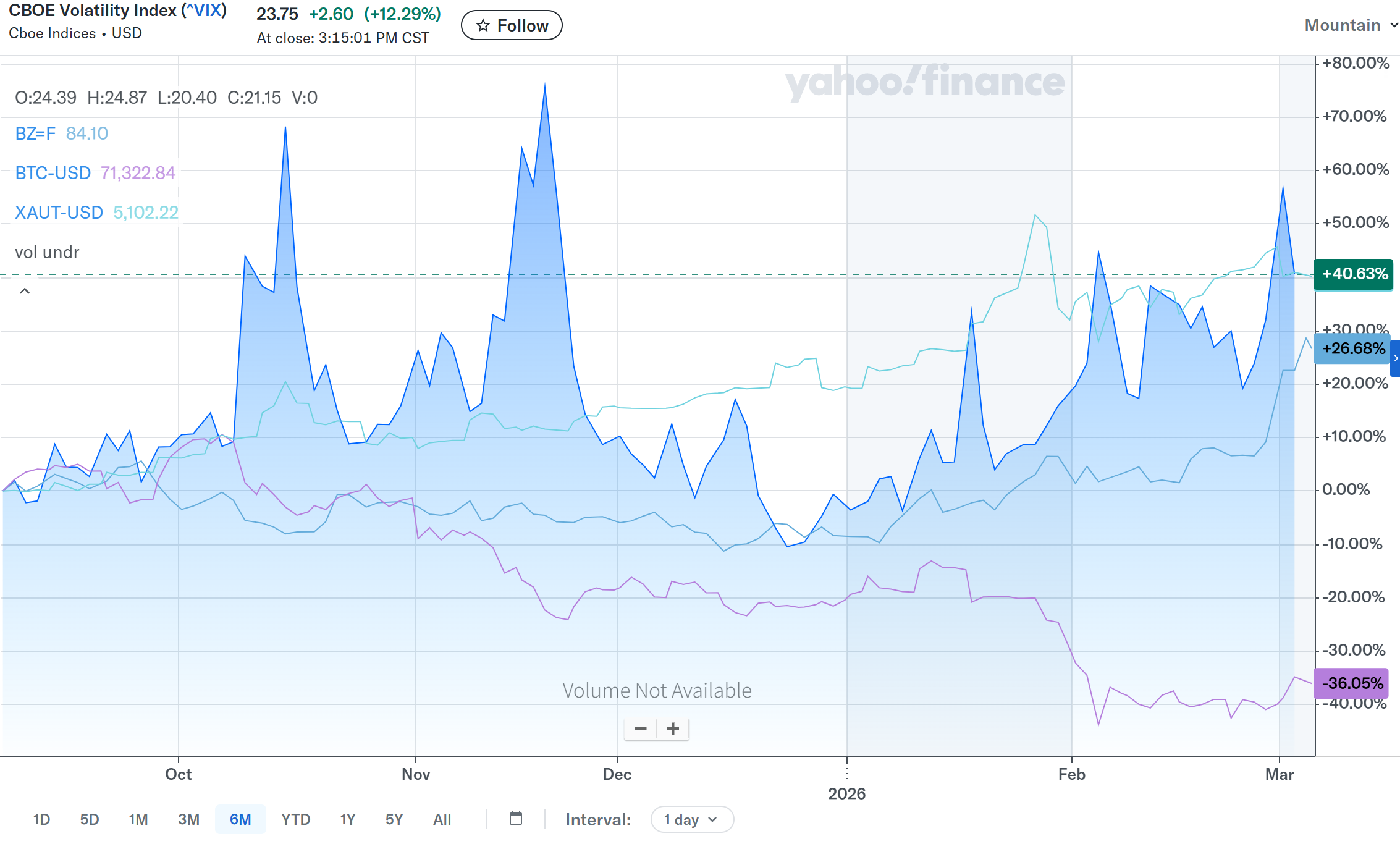

The chart below illustrates the six-month trend compiled by Yahoo Finance. The blue shaded area represents the CBOE Volatility Index (VIX), while the performance of Brent crude oil futures, gold, and Bitcoin is overlaid for comparison. As geopolitical risks escalated in 2026, the VIX rose significantly. On March 6, 2026, it closed at 23.75, while Brent crude oil rebounded strongly. Gold, as a safe-haven asset, recorded a notable increase, while Bitcoin experienced a sharp pullback.

This chart clearly illustrates the dual transmission channel of geopolitical risk: “VIX surge + energy price surge.” On one hand, it increases market volatility and inflation expectations; on the other hand, it places significant pressure on high-beta risk assets such as cryptocurrencies.

Source: https://finance.yahoo.com/

III. Reasons for High Beta of Encrypted Assets

Many people describe Bitcoin (BTC) as “digital gold,” but in most macro environments, it behaves more like a highly volatile version of the Nasdaq. The main reasons can be explained through a three-layer structure: the inclusion of crypto in risk asset correlation frameworks, the dominance of derivatives in price discovery, and the endogenous liquidity cycle driven by stablecoins and exchange margin systems.

-

Risk Asset Correlation

Research from CME Group shows that the correlation between crypto assets and the NASDAQ 100 has remained positive for a prolonged period since 2020. During certain phases in 2025 and early 2026, the rolling correlation ranged from approximately 0.35 to 0.60, though this relationship is clearly cyclical rather than constant.

[图片上传中...]

Source: https://www.cmegroup.com/insights/economic-research/

This means that, once a macro shock triggers broad risk-asset reduction, such as war escalation, rising oil prices, or delayed interest rate cut expectations, BTC rarely moves independently and often declines even faster. This dynamic represents the first layer of crypto’s “high beta” characteristic.

-

High Leverage Amplifies Volatility

Sharp price swings in the cryptocurrency market are often driven not by immediate changes in fundamentals but by chains of funding rates, margin dynamics, and forced liquidations that accelerate deleveraging.

During the “10/11” market crash in 2025, more than $19 billion in leveraged positions were liquidated within 24 hours, setting a record for the largest single-day liquidation in crypto history. At the same time, perpetual contract positions did not significantly contract beforehand, suggesting that forced liquidation cascades can push an already fragile market into non-linear price movements.

-

Endogenous Mobility Mechanism

When expectations of macro tightening rise, stablecoin liquidity becomes more cautious, while borrowing and margin conditions tighten simultaneously. This creates a self-reinforcing liquidity contraction cycle:

Available margin decreases → forced position reductions → price declines → collateral values shrink → further forced reductions.

Unlike traditional financial markets, which rely heavily on central bank liquidity injections or withdrawals, the crypto market operates more like a system that automatically contracts liquidity under stress, making it more prone to sharp declines and rapid rebounds.

So, is the “digital gold” narrative still valid? Historically, the peak rolling correlation between BTC and gold has been limited and has fallen close to zero since 2024. A more accurate framework may be:

-

Short term: BTC behaves like a high-beta risk asset during macro shocks.

-

Medium to long term: Under structural scenarios such as capital controls, cross-border financial frictions, or sovereign credit stress, BTC may increasingly reflect its narrative as a borderless settlement asset with non-dilutive supply characteristics.

IV. Outlook for Future Trends

The impact of geopolitics on crypto markets is essentially not about whether war benefits Bitcoin, but rather about how risk appetite and liquidity conditions evolve. While the situation in the Middle East remains uncertain, we outline three potential scenarios to assess possible paths, key triggers, and corresponding market trends.

-

Base Scenario: Shock Repair

Assuming the conflict remains within a controllable range and does not lead to long-term disruptions in key shipping routes or energy supply, oil prices may remain elevated but stop trending upward. In this case, the market’s secondary concerns about inflation would gradually ease, the VIX would decline, and interest rate cut expectations could slowly recover as macro data improve.

In such an environment, crypto—as a high-beta asset—may not immediately enter a strong unilateral trend. Instead, it is more likely to follow a “range-bound consolidation followed by gradual recovery” pattern. Downside support may emerge from risk premium compression and dip-buying interest, while macro uncertainty and slow leverage recovery could limit the pace of upside momentum.

-

Pessimistic Scenario: Double Bottom

If the conflict expands further—leading to significant supply disruptions or sustained increases in shipping costs—oil prices could continue rising, triggering renewed inflation pressures. This would likely force the market to delay interest rate cuts further or even reprice higher real interest rate paths, resulting in broader valuation pressure across risk assets.

Under such conditions, crypto’s triple amplification effect may emerge: Declining risk assets + derivatives deleveraging + endogenous liquidity contraction (tighter margin and lending conditions).

This combination could create a market structure characterized by accelerating declines, weak rebounds, and renewed breakdowns, forming the classic double-bottom pattern.

-

Optimistic Scenario: High Volatility Excess Rebound

If geopolitical tensions cool quickly, oil prices fall, the VIX declines, and macro indicators signal clearer monetary easing, market confidence in the interest rate-cut path could recover rapidly, restoring risk appetite.

In this scenario, the crypto market may display strong rebound elasticity. Capital inflows, short covering, and renewed leverage could drive a sharp upward move in prices. However, investors should remain cautious: the structural characteristics of the crypto market mean it often rises quickly but also corrects quickly, making it vulnerable to sharp pullbacks when market sentiment becomes overheated.

V. Inspiration and Summary

Cryptocurrencies have become deeply integrated into the global macro-financial cycle and are no longer independent “narrative assets” operating outside the mainstream. Instead, they increasingly behave as high-beta risk assets influenced by oil prices, inflation expectations, interest rate paths, and market volatility.

Three Key Insights

Insight 1: The real impact of geopolitical risk lies in the advance pricing of “threat” risk premiums

After the GPR index separates geopolitical risk into “threat” and “action” phases, empirical evidence shows that negative market effects are largely driven by the former. Markets often begin repricing risk before conflicts fully materialize, through signals such as rising VIX levels, oil risk premiums, and shifting interest rate expectations. In this sense, expectations gradually become reality through market pricing.

Insight 2: The high-beta characteristics of crypto markets are the combined result of macro transmission and market structure

Risk appetite shifts, inflation and interest rate expectations, and liquidity repricing interact with crypto-specific structural features, such as 24/7 trading, high leverage, forced liquidations, and endogenous liquidity cycles. Together, these forces amplify volatility, making crypto assets significantly more sensitive to macro shocks than traditional markets. This dynamic is structural rather than purely sentiment-driven.

Insight 3: Bitcoin’s integration into the macro financial system has become an irreversible trend

Bitcoin and US equity markets have developed a long-term positive correlation, suggesting that Bitcoin is increasingly traded as a risk-sensitive macro asset. In the short term, Bitcoin often behaves more like a high-volatility version of the Nasdaq. Over the medium to long term, however, in scenarios involving capital controls, sovereign credit crises, or intensified cross-border financial frictions, Bitcoin may more clearly exhibit the characteristics of “digital gold.”

Conclusion

In the current environment of high interest rates and escalating geopolitical tensions, Bitcoin’s “digital gold” narrative is temporarily overshadowed by its high-beta risk characteristics. Investors who understand the transmission mechanisms of geopolitical risk can shift from passively enduring market volatility to actively identifying opportunities.

By translating geopolitical uncertainty into quantifiable risk premiums and liquidity signals and dynamically evaluating their impact on asset allocation, investors can make more rational decisions in complex market environments. The long-term value of the cryptocurrency market does not lie in avoiding macro cycles, but in understanding them deeply and positioning accordingly.

About Us

Hotcoin Research, the core research and investment arm of Hotcoin Exchange, is dedicated to turning professional crypto analysis into actionable strategies. Our three-pillar framework—trend analysis, value discovery, and real-time tracking—combines deep research, multi-angle project evaluation, and continuous market monitoring.

Through our Weekly Insights and In-depth Research Reports, we analyze market dynamics and highlight emerging opportunities. With Hotcoin Selects—our exclusive dual-screening process powered by both AI and human expertise, we help identify high-potential assets while minimizing trial-and-error costs.

We also engage with the community through weekly livestreams, decoding market hot topics, and forecasting key trends. Our goal is to empower investors of all levels to navigate cycles with confidence and capture long-term value on Web3.

Risk Disclaimer

The cryptocurrency market is highly volatile, and all investments carry inherent risks. We strongly encourage investors to remain informed, assess risks thoroughly, and adhere to strict risk management practices to protect their assets.

Connect with Us

Website:https://www.hotcoin.com/en_US/learn/index/

X: x.com/HotcoinAcademy

Email: labs@hotcoin.com

Lettura consigliata

Visualizza altro

Hotcoin Research | Playing and Earning in WEB3: The Secrets Behind Millions in Funding: How Sonic is Changing the Solana Gaming Ecosystem

In-depth Research

Hotcoin Research | WEB3 Earnings: Farcaster: Ushering in a New Era of Decentralized Social Networks

In-depth Research

Hotcoin Research | Unlocking Trillions: How the U.S. 401(k) Pension Plan Could Drive the Next Long-Term Crypto Bull Market

In-depth Research