Hotcoin Research | Telegram Takes Over TON: Can a Billion-User Gateway Truly Lift the On-Chain Ecosystem?

TL;DR

Background: Telegram founder said Telegram will replace TON Foundation as TON's driving force, drawing market attention.

TON's history: Telegram-native project - separated after SEC allegations - continued by the community - embedded into products - deep participation in organization and infrastructure.

Ecosystem status: the application layer is stronger than the financial layer, user acquisition is stronger than asset retention, and the payment narrative is stronger than actual on-chain monetization.

Opportunity highlights: payment and stablecoin scenarios | advertising and the creator economy | Mini Apps and games | AI Agent and Bot economy.

Risk highlights: centralization risk | regulatory risk | application quality and value capture risk | DeFi depth is insufficient to support large-scale financial activity.

Conclusion: Whether Telegram can truly propel TON depends on whether it can convert Telegram’s social user base into a self-sustaining on-chain economy.

On May 4, 2026, Pavel Durov, the founder of Telegram, posted on X that TON fees have dropped sixfold to near zero; next, Telegram will replace the TON Foundation as the driving force of TON and become the largest validator of TON; in the next 2-3 weeks, the focus will be on rolling out the new ton.org, new developer tools and performance upgrades. This event quickly changed the market's pricing logic for TON. In the past, TON's core narrative was "a blockchain network closely related to Telegram"; now, the market is beginning to re-evaluate whether it will become "an on-chain consumption and payment network directly driven by Telegram". So, can Telegram's formal takeover truly push TON beyond a user-growth narrative toward verifiable ecosystem growth?

I. TON’s Origins: Separation and Reintegration

The TON network was originally conceived as the Telegram Open Network, designed to support high-frequency payments, applications, and digital asset use cases at Telegram scale. In 2019, Telegram raised $1.70 billion through its initial coin offering (ICO) to develop TON. The SEC subsequently accused Telegram of selling Gram tokens as unregistered securities, violating US securities laws. In 2020, Telegram reached a settlement with the US SEC, returning about $1.20 billion and paying a fine of $18.5 million. Telegram was forced to stop the original TON project, and TON was continued and developed by the community and foundation. This history has kept TON in a delicate state for a long time: it has Telegram lineage, but it is not completely equivalent to Telegram’s official blockchain.

The real turning point in the relationship came after Telegram's product ecosystem began to go on-chain. Since 2023, Telegram Mini Apps, Telegram Wallet, Telegram Stars, ad revenue sharing, and bot ecosystem have gradually formed a new monetization loop, and TON has regained the opportunity to embed in Telegram's product system. By January 2025, the relationship between TON Foundation and Telegram had reached a key turning point: TON Foundation announced that TON will become the exclusive blockchain infrastructure for the Telegram Mini Apps ecosystem, and TON Connect will become the exclusive protocol for Telegram Mini Apps to connect to blockchain wallets. Meanwhile, Toncoin will continue to be used for non-USD payment and ecosystem settlement scenarios, including Telegram Stars, Premium, Ads, and Gateway. This means that the relationship between TON and Telegram has evolved from a historical connection into deep product integration.

Durov's tweet further pushed this partnership to the organizational and infrastructure levels. The market's attention is not just because Durov once again "supports TON", but because it has reshaped how the market evaluates TON.

-

Telegram becomes the largest validator: This means that it is no longer just a distribution channel for TON, but directly expands into network security, node governance, and infrastructure operations. For a blockchain network focused on high-frequency payments and Mini Apps use cases, the change in the role of a validator represents a significant increase in Telegram's participation in the chain itself.

-

Telegram replaces TON Foundation as the main driving force: TON's development focus may shift from foundation-led ecosystem expansion to growth increasingly driven by real use cases within Telegram’s ecosystem. In the future, TON's growth logic may no longer mainly rely on external DeFi ecosystems, gaming projects, or early-stage on-chain ventures, but more on whether Telegram's internal products can continue to create demand for payment, advertising, subscriptions, developer revenue sharing, and Mini Apps transactions.

-

The new official website, new developer tools, and performance upgrades provide a near-term delivery window: The market is no longer trading solely on Telegram’s billion-user reach, but is beginning to pay attention to whether Telegram can really improve TON's developer experience, network performance, and application conversion efficiency in the short term, so that TON's narrative can move from long-term upside potential to near-term execution.

From the perspective of market performance, the market reaction in TON’s price was quite direct. According to CoinGecko data, before and after Durov's post, TON quickly rallied from around $1.60 and then rose to around $2.90 in the subsequent market, with a gain of nearly 80%. TON has since retraced to around $2.08, with market enthusiasm cooling significantly from the peak. This means the market has essentially completed the first round of narrative-driven pricing for the event: short-term funds are trading the narrative premium driven by the strengthening of the relationship between Telegram and TON, rather than the full realization of fundamental results. As the price falls from its high, TON's trading logic is shifting from narrative pricing to execution validation. The subsequent market focus will no longer be just on Durov's statement itself, but whether Telegram can truly bring sustained user conversion, sustained growth in on-chain activity, ecosystem revenue growth, and a clearer monetization model to TON.

II. TON Ecosystem Data: Assessing the Real Fundamentals

Telegram is TON’s largest user acquisition channel, but on-chain data determines whether TON can move from a user narrative to a financial network. Telegram's MAUs exceed 1 billion, but social media users do not automatically translate into on-chain users, and chat users are not naturally equal to wallet users. What TON really needs to prove is whether Telegram’s distribution reach can be converted into wallet activation, transaction frequency, stablecoin adoption and retention, DeFi usage, and developer income.

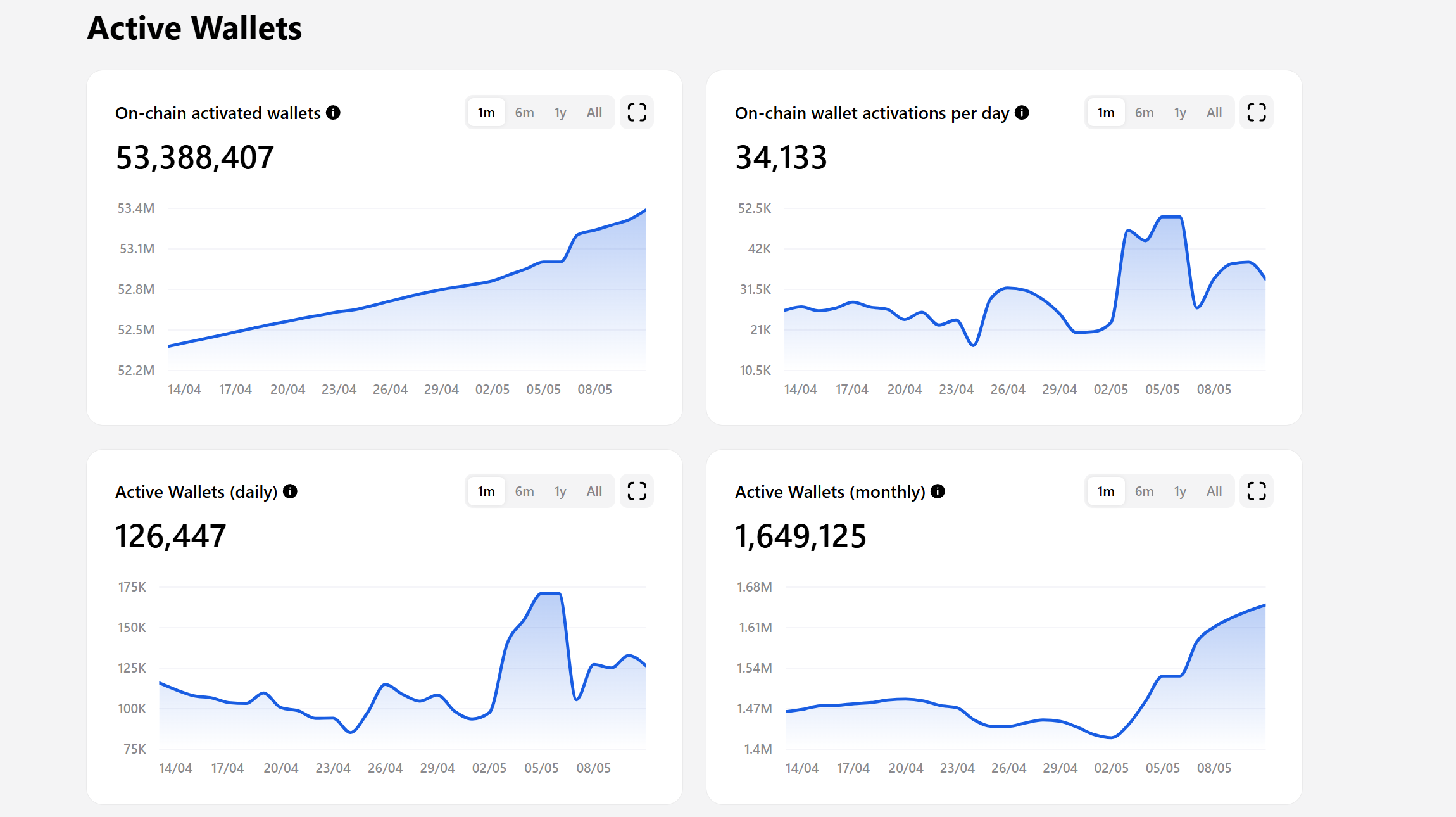

According to TON Stat data, as of May 14, 2026, the number of TON on-chain accounts is about 181.70 million, the number of active wallets is about 53.39 million, daily active wallets totaled approximately 126,400, and the number of transactions on the day is about 3.4392 million. This shows that TON already has a sizable wallet and account base, but truly high-frequency and sustainable on-chain activity still falls short of the expectations implied by Telegram’s billion-user reach.

Source: https://www.tonstat.com/

At the validator level, TON Stat showed on May 14th that the number of validators was 417, and validators had staked approximately 598.6 million TON. This indicates that TON already has a large-scale staking security layer. If Telegram further becomes the largest validator, the endorsement of network security will increase, but concerns around centralization would likely intensify as well.

Source: https://www.tonstat.com/

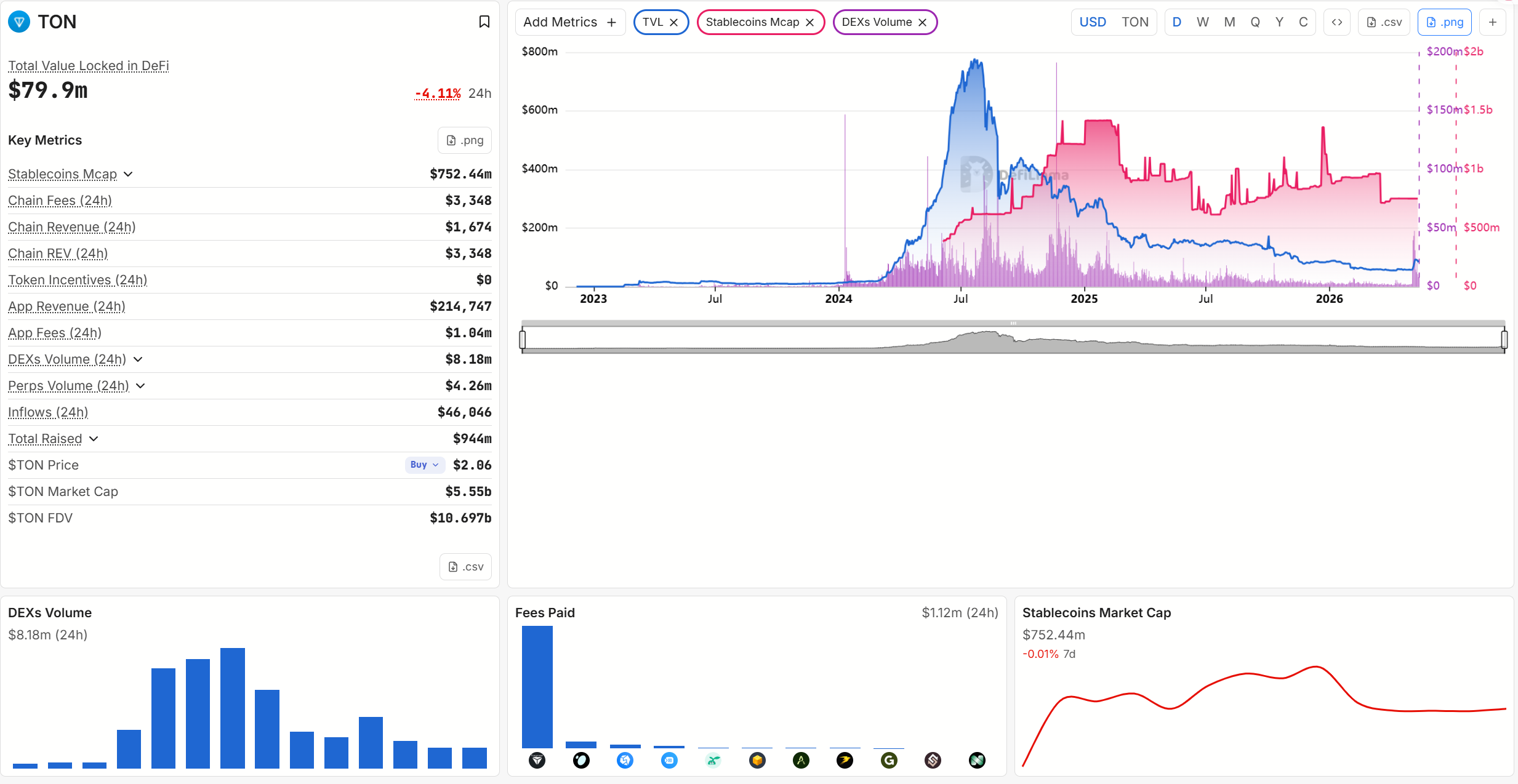

More importantly, the key issue is capital retention. According to DeFiLlama data, as of May 14, 2026, TON’s DeFi TVL is about $79.43 million, and the DEX volume is only $8.18 million; the total supply of stablecoins is about $752 million, of which USDT is about $580 million and Ethena USDe is about $171.90 million. This comparison is crucial: the scale of stablecoins is significantly higher than that of DeFi TVL, indicating that TON's payment flows and capital inflows have a foundation, but DeFi's composability, lending depth, yield opportunities, and institutional-level liquidity have not yet been fully released.

Source: https://defillama.com/chain/TON

III. Representative Projects: From Mini App User Growth to On-Chain Financial Infrastructure

The core feature of the TON ecosystem is not simply copying the Ethereum-style DeFi path, but forming a relatively unique growth chain around Telegram's social distribution capabilities: first acquiring users through Mini Apps, then acquiring assets through wallets, stablecoins, DEX, lending, staking, and derivatives, and ultimately attempting to transform Telegram’s social user base into a self-sustaining on-chain economy. Therefore, observing the TON ecosystem cannot only focus on TVL, but also on user scale, payment scenarios, asset retention, and financial infrastructure maturity.

1. Telegram Native App: Strong Distribution Advantage, But Retention Still Needs to Be Verified

The most recognizable type of project in the TON ecosystem is the consumer-facing application based on Telegram Mini Apps, especially Tap-to-Earn, mini-games, and lightweight Web3 interactive products. The advantages of this type of project are immediately apparent: users do not need to download independent apps, they can directly complete access, interaction, wallet connection, and task participation within Telegram, significantly lowering the onboarding friction for Web3 applications.

-

Notcoin: Through a minimalist click mechanism, it rapidly expanded its user base within Telegram, reaching about 35 million users and accumulating about 2.8 million on-chain holders. The significance of Notcoin lies not only in the success of a single game, but also the first proof point that Telegram Mini Apps can serve as a Web3 user onboarding layer, transforming traditional social platform users into on-chain addresses and token holders.

-

Hamster Kombat: This pushed the model to viral scale. The official claims to have more than 300 million players, and through gamification tasks, channel subscriptions, video dissemination, and potential airdrop expectations, it has achieved strong viral distribution. It verifies the distribution efficiency of Telegram and amplifies the controversy of the Tap-to-Earn model: user growth can be extremely fast, but how many of them are real high-value users, whether they can be retained after airdrops, and whether they can be converted into long-term on-chain behavior still need subsequent data verification.

-

Catizen: Represents a more monetized type of Mini App. Catizen has over 39 million users, over 18 million MAUs, and has become the first consumer-facing Web3 application to break through 1 million paying users. Compared to Notcoin and Hamster Kombat, Catizen's selling point is not just about attracting new users, but also its monetization capability and centralized game operations capability, which makes it closer to the "consumer application + Web3 incentive" model within the Telegram ecosystem.

However, this type of project also exposes the first challenge of the TON ecosystem: user acquisition can scale rapidly, but retention and capital retention remain difficult. Tap-to-Earn can bring users into the wallet, task, and airdrop system, but engagement can drop sharply after the TGE or airdrop ends. If the TON ecosystem only stays in the cycle of "game acquisition - token issuance - user exit", what Telegram provides will only be short-term attention, not sustainable network effects. The key question is whether projects like Notcoin, Hamster Kombat, and Catizen can continue to guide users towards higher-frequency scenarios such as payment, trading, staking, lending, consumption, and content payment.

2. DEX and Transaction Infrastructure: The First Layer of TON’s On-Chain Financial Stack

Source: https://defillama.com/chain/TON

Once Mini Apps drive user acquisition, TON needs to rely on DeFi and liquidity infrastructure to support asset flows. According to DeFiLlama data, as of May 14, 2026, the 24-hour DEX trading volume on the TON chain is about $8.18 million, and the 7-day trading volume is about $145 million; the 24-hour Perps trading volume is about $4.55 million, and the 7-day trading volume is about $23.09 million. This shows that TON has already developed a baseline level of on-chain trading activity, but compared with Telegram’s mass-adoption narrative, its financial depth is still in the early stage.

-

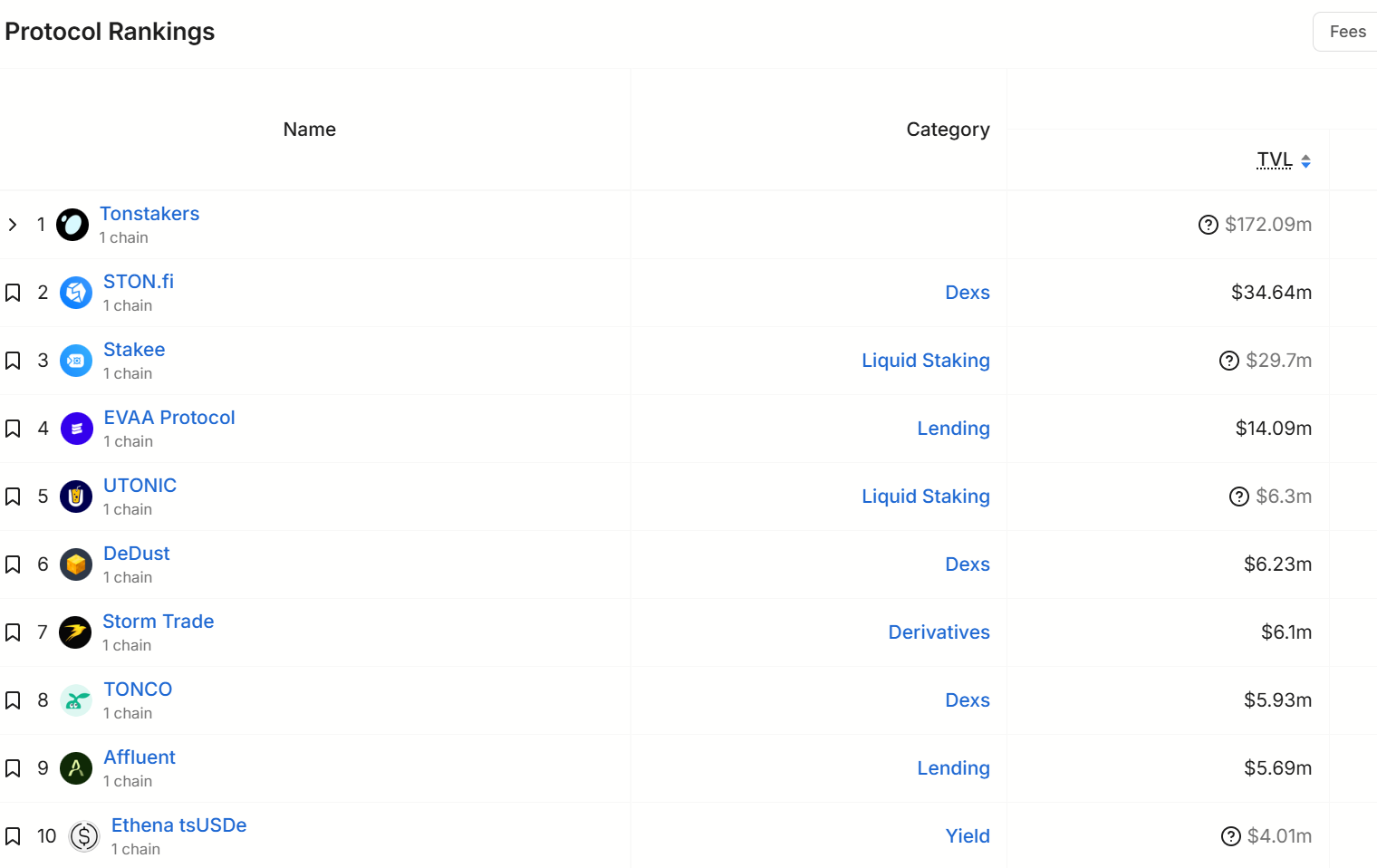

Liquid staking yield layer: Tonstakers is the core project of TON's liquidity staking track. LSD TVL is about $172.10 million, mainly tokenizing TON's staking income, providing basic assets for subsequent collateral, trading, and yield strategies. Stakee TVL is about $29.7 million, together with Tonstakers, bemo, UTONIC, etc., forming TON's staking income layer, reflecting that users are not only concerned about trading TON, but also beginning to look for native yield opportunities.

-

DEX trading infrastructure: STON.fi TVL is about $34.64 million, which is a well-known AMM protocol in the TON ecosystem, responsible for ecosystem asset exchange, liquidity pool, and trading routing functions. DeDust TVL is about $6.23 million, more oriented toward a community-native trading layer, supporting a wide range of long-tail assets within the TON ecosystem, but also facing liquidity dispersion and slippage issues. TONCO TVL is about $5.93 million, further enriching TON's trading routing and fee revenue structure.

-

In terms of lending and derivatives: EVAA Protocol TVL is about $14.09 million, representing the TON lending market and supplementing the use of collateral lending and stablecoins. Storm Trade TVL is about $6.1 million, focusing on on-chain leverage and derivative trading, which helps to improve trading activity level, but requires higher liquidity, oracles, and clearing mechanisms.

Overall, TON DeFi has initially formed a basic structure of "staking yield - DEX trading - lending - derivatives", but the core challenge remains: strong user acquisition and weak capital retention. Whether the value of the ecosystem can be further expanded in the future depends on the depth of stablecoins, the supply of high-quality assets, and whether Mini Apps users can be transformed into real on-chain trading, lending, and yield-seeking users.

3. Stablecoins and Cross-Chain Assets: The Key to TON’s Transition from a Distribution-Driven Chain to a Payment Network

Stablecoins are one of the most important underlying assets in the TON ecosystem. Telegram's internal payments, tipping, ad revenue sharing, developer settlements, cross-border transfers, and Mini Apps monetization all require stable pricing units rather than relying entirely on TON's local currency fluctuations.

Currently, the most important stablecoin asset on TON is USDT. According to DeFiLlama stablecoin data, the total market value of stablecoins on the TON chain is about 752 million US dollars, of which USDT is about 580 million US dollars, accounting for about 77%. The significance of USDT to TON is not only to improve trading liquidity, but more importantly, it makes it possible for "digital dollar transfers" within Telegram, providing a basic settlement unit for wallets, payments, merchant collections, and cross-border remittances.

Besides USDT, Ethena USDe has also become one of the important stable assets on TON. According to DeFiLlama data, the scale of USDe on TON is about 172 million US dollars. The introduction of USDe has enabled TON not only to have payment-focused stablecoins, but also to begin to access yield-bearing dollar assets, providing greater composability for subsequent DeFi income, collateralized lending, and structured products.

These stablecoins and cross-chain assets are the key to TON's upgrade from a social-focused blockchain to a payment settlement network. If in the future USDT, USDe, potential BTC mapping assets, and more cross-chain assets can integrate into a broader economic flywheel around Telegram Wallet, Mini Apps, advertising revenue, creator sharing, and DeFi revenue layer, TON's value capture logic will no longer be just about on-chain gas and transaction fees, but will expand to payment flows, asset retention, capital retention, and platform-level application revenue.

Overall, the current ecosystem pattern of TON can be summarized as follows: the application layer is stronger than the financial layer, the distribution is stronger than capital retention, and the payment potential currently outweighs actual monetization and asset retention. Telegram provides TON with a distribution advantage that is difficult for other blockchain networks to replicate, which is TON's biggest structural advantage. However, what TON really wants to prove is not "whether it can bring users", but "whether it can make users leave assets, generate transactions, complete payments, and continue to consume". If these dynamics hold, TON’s positioning could evolve from a “Telegram-driven growth narrative” into a “Telegram-native financial network”; if they fail to materialize, TON may remain an attention-driven ecosystem for a long time, relying on viral applications and events to stimulate cyclical growth.

IV. Opportunities and Challenges: Can a Billion-User Portal Transform into a Sustainable Network Effect?

The seven-step upgrade plan (MTONGA) proposed by Durov in April 2026, namely Make TON Great Again. The core includes improving TON performance, reducing transaction costs, improving block generation and confirmation speed, strengthening Telegram's participation in TON's infrastructure, and gradually improving developer tools, official websites, and ecosystem access points. The goal is to make TON more suitable for Telegram-scale high-frequency payments, Mini Apps, Bot, and AI Agent scenarios.

1. Opportunities: What Real Incremental Benefits Can Telegram Bring to TON?

After Telegram took over TON, the market's most valued opportunities mainly came from four directions.

First, payment and stablecoin scenarios. Telegram is a natural cross-border communication tool with users distributed globally and strong community attributes in many Emerging Markets. If TON can achieve low-cost transfer, merchant payment, P2P remittance, digital commodity purchase and stablecoin settlement within Telegram, it could offer a payment channel much closer to real users than most traditional DeFi ecosystems. In the past, TRON obtained a stablecoin network effect through low-cost USDT transfer. The difference with TON is that it may embed stablecoin transfers into social relationships, rather than just staying between exchanges and wallets.

Second, advertising and creator economy. The Telegram ad platform has formed a certain payment relationship with TON. Channel owners, content creators, and developers can earn revenue through Telegram's advertising, Stars, and application revenue. If these revenues are settled in TON ecosystem assets, it will form a continuous demand and redistribution cycle. Advertisers purchase services, the platform distributes revenue, creators earn revenue, and users consume content. This process may become the most realistic cash flow scenario for TON.

Third, Mini Apps and games. Projects such as Notcoin, Hamster Kombat, and Dogs from 2024 to 2025 have proven that Telegram Mini Apps can reach a large number of users in a very short period of time. However, early cases have also exposed problems: fast user growth, strong token hype, but retention, consumption, and long-term income may not be stable. After Telegram takes over TON, if it can guide Mini Apps from "click mining" to games, content, e-commerce, task platforms, and financial applications through better developer tools, wallet experience, and app review system, the quality of TON's ecosystem will truly improve.

Fourth, AI agents and the bot economy. Telegram itself is a highly active platform for bots. If AI agents undertake functions such as customer service, transaction assistant, content generation, task execution, and payment settlement in Telegram in the future, then low-cost on-chain wallets and smart contract accounts may become the payment and coordination layer of AI agents. TON Strategy also mentioned in its Q1 2026 conference call that TON's account model and Telegram distribution scenarios may be suitable for AI agents to directly perform payment and service interactions in chat, bot, or Mini Apps. Although this direction is still in its early stages, it may be the most imaginative part of the combination of Telegram and TON.

Telegram provides initial distribution advantages that are difficult for other blockchain ecosystems to replicate, but TON needs to transform these distribution advantages into payments, applications, assets, and developer revenue. Only by completing this transformation can TON move from a user-growth narrative to financial infrastructure.

2. Challenges: Telegram’s Deep Involvement Increases Pressure on TON

Telegram's takeover is not an unconditional benefit. It improves execution, but also increases responsibility and risk exposure.

The first challenge is centralization risk. Telegram becoming the largest validator will strengthen execution and network security, but it will also weaken TON's decentralized narrative. If the validator's weight, key upgrades, and ecosystem resources rely too much on Telegram, TON will be more like a "platform-controlled blockchain" rather than a fully neutral and open blockchain network.

The second challenge is regulatory risk. Telegram has reached a settlement with the SEC over the issuance of Gram tokens, which is still a long-term burden for TON. Now that Telegram is deeply involved in TON again, although the path is no longer the direct issuance of Gram tokens, the boundaries between payments, earnings, stablecoins, wallets, and user assets may still attract regulatory scrutiny.

The third challenge is application quality and value capture. Notcoin, Hamster Kombat, and Catizen have proven that Telegram can create explosive products, but whether it can retain stablecoin balances, borrowing demand, paying users, and developer income after explosive products is the real test. If a large number of applications only use stablecoins or internal reward points, and TON only bears low-cost gas, TON's value capture may be lower than market expectations.

The fourth challenge is insufficient DeFi depth. Compared with mature ecosystems such as Ethereum, Solana, and Base, TON’s on-chain DeFi sector remains in an early stage. Overall TVL remains relatively small, while liquidity is concentrated in a limited number of DEXs, liquid staking, and lending protocols, with fragmentation still evident across major platforms. Although TON has already established core modules such as trading, staking, lending, and derivatives, key areas including stablecoin depth, asset diversity, trading slippage, lending utilization, and liquidation liquidity still require significant improvement. At its current stage, TON’s DeFi infrastructure is not yet capable of supporting large-scale and sophisticated on-chain financial activity.

In short, MTONGA provides short-term catalysts for performance upgrades and platform collaboration, while payment and stablecoins, Mini Apps, developer sharing, and Bot/AI Agent scenarios constitute long-term upside potential. However, Telegram's deep involvement also brings risks of centralization, regulation, and platform dependence. Currently, TON's DeFi depth and asset accumulation ability are still insufficient to fully support large-scale financial activities. Therefore, what TON really needs to verify in the next stage is its conversion ability from "user entry" to "capital retention", from "viral applications" to "sustained income", and from "ecosystem narrative" to "network effects".

V. Outlook and Conclusion: Can TON be truly propelled by Telegram?

To determine whether Telegram can truly propel TON, five key variables need to be observed.

Firstly, whether Telegram has truly entrusted its core business scenarios to TON. Advertising, Stars, Premium, Gateway, Mini Apps, digital gifts, stickers, channel revenue, and developer revenue sharing, if continuously settled with TON or TON ecosystem assets, TON's demand will be more stable. If these scenarios are only partial pilots, TON's value capture will be limited.

Secondly, whether the wallet users continue to grow and remain active. The key to TON is not how many MAUs Telegram has, but how many users actually open the wallet, complete on-chain payments, use Mini Apps, purchase digital assets, and participate in on-chain applications. Wallet activation, monthly active wallets, transaction frequency, and retention rates are more important than just Telegram MAU.

Thirdly, whether the developer ecosystem has shifted from growth hacking to real applications. Short-term projects can generate hype, but long-term ecosystems need sustainable products. TON needs more real revenue-generating applications, such as payment tools, games, subscriptions, content economy, AI Bot, stablecoin services, on-chain identity, and lightweight DeFi.

Fourth, whether liquidity and assets remain within the ecosystem. Trading volume and user numbers are only superficial indicators. The scale of stablecoins, DeFi TVL, staking ratio, application revenue, transaction fees, active developers, and long-term asset retention are deeper indicators. If TON is only active in high-frequency but low-value transactional activity, and the asset accumulation is insufficient, its Layer 1 valuation would still remain constrained.

Fifth, whether the governance and validator structure is transparent. After Telegram becomes the largest validator, the market needs to see greater transparency around validator distribution, staking scale, governance process, changes in foundation roles, and technology roadmap disclosure mechanism. Only with increased transparency can Telegram's strong control not be transformed into a centralization discount.

Therefore, whether Telegram can truly propel TON will not be determined by a single 100% rally. More accurately, this event has pushed TON from a "Telegram-themed asset" to a "Telegram infrastructure asset" repricing stage. If Telegram can deliver on low fees, high performance, developer tools, stablecoin payments, and ecosystem governance transparency, TON has the opportunity to become the on-chain consumer network closest to the general public. If the follow-up only stays in slogans, short-term games, and centralized validator disputes, TON may still return to the old path of high-volatility narrative assets.

Conclusion

The essence of Telegram taking over TON is a key turning point for the TON ecosystem to move from an "external cooperation chain" to an "Telegram’s native financial infrastructure". Telegram does provide a distribution advantage that other blockchain ecosystems cannot easily replicate for TON, but a distribution advantage does not guarantee ecosystem success. For TON, the real challenge is to transform Telegram's user relationships into on-chain wallets, transform wallets into payments and applications, transform applications into sustainable revenue and asset retention, and then transform these revenues and asset retention into long-term value capture for Toncoin. If any link in this process breaks, TON may remain in the stage of "strong narratives but limited capital retention".

Therefore, whether Telegram can truly propel TON depends on whether Telegram can continue allocating product, distribution, developer, and validator resources to TON in a transparent and disciplined manner, while avoiding excessive centralization and regulatory backlash. What really needs attention is not Telegram's takeover itself, but whether TON can build a verifiable and self-sustaining on-chain economy after the takeover.

About Us

Hotcoin Research, the core research and investment arm of Hotcoin Exchange, is dedicated to turning professional crypto analysis into actionable strategies. Our three-pillar framework—trend analysis, value discovery, and real-time tracking—combines deep research, multi-angle project evaluation, and continuous market monitoring.

Through our Weekly Insights and In-depth Research Reports, we analyze market dynamics and highlight emerging opportunities. With Hotcoin Selects—our exclusive dual-screening process powered by both AI and human expertise, we help identify high-potential assets while minimizing trial-and-error costs.

We also engage with the community through weekly livestreams, decoding market hot topics, and forecasting key trends. Our goal is to empower investors of all levels to navigate cycles with confidence and capture long-term value on Web3.

Risk Disclaimer

The cryptocurrency market is highly volatile, and all investments carry inherent risks. We strongly encourage investors to remain informed, assess risks thoroughly, and adhere to strict risk management practices to protect their assets.

Connect with Us

Website:https://www.hotcoin.com/en_US/learn/index/

X: x.com/HotcoinAcademy

Email: labs@hotcoin.com

Inirerekumendang pagbabasa

Tingnan ang higit pa

Hotcoin Research | Guide to Investing in Meme Coins: A Safety Manual for Survival

In-depth Research

Hotcoin Research | Play and Profit in WEB3: Movement Labs Unveiled—A Cross-Revolution of Move Language and EVM

In-depth Research

Hotcoin Research | The DeFi 0 Threshold Era Is Coming: Observations and Analysis of the Abstraction and Intention Tracks

In-depth Research

Mga contact sa serbisyo

Service@hotcoin.com

Feedback ng produkto

Product@hotcoin.com

Kooperasyon sa negosyo

Business@hotcoin.com

Legal na mga contact

Casecn@hotcoin.com

Tungkol sa atin

produkto

maglingkod

suporta

©2017-2026